First-Time Homebuyer’s Guide to Buying a House in Texas

Buying your first home is exciting—but let’s be honest, it can also feel overwhelming. Between figuring out your budget, understanding loans, and navigating the Texas housing market, many first-time buyers don’t know where to start.

Buying your first home is exciting—but let’s be honest, it can also feel overwhelming. Between figuring out your budget, understanding loans, and navigating the Texas housing market, many first-time buyers don’t know where to start.

The good news? You don’t have to figure it out alone.

Whether you’re a renter ready to stop paying someone else’s mortgage, a military family relocating to Texas, or simply dreaming about owning your first home, this guide will walk you through the homebuying process step by step.

By the end of this article, you’ll understand what it takes to buy a home in Texas and how to avoid common mistakes first-time buyers make.

Why Buying a Home in Texas Makes Sense

Texas continues to attract homebuyers from across the country—and for good reason.

Here are a few benefits of buying a home in Texas:

-

No state income tax

-

Strong job market and growing economy

-

Affordable housing compared to many other states

-

Opportunities to build long-term wealth through equity

-

Great communities for families and military relocation

For renters, buying a home can also mean stable monthly payments instead of rising rent prices year after year.

Step 1: Understand Your Budget

Before looking at homes online, the first step is understanding how much house you can comfortably afford.

Many first-time buyers focus only on the monthly mortgage payment, but there are additional costs to consider:

-

Property taxes

-

Homeowners insurance

-

HOA fees (if applicable)

-

Utilities

-

Maintenance and repairs

A lender can help you determine your buying power through a pre-approval process. This gives you a clear price range and strengthens your offer when you find the right home.

Pro Tip:

Avoid buying at the very top of your budget. Leave room for emergencies, savings, and lifestyle expenses.

Step 2: Check Your Credit Score

Your credit score plays a major role in:

-

Loan approval

-

Interest rates

-

Monthly payment amount

Generally:

-

620+ is often needed for conventional loans

-

FHA loans may allow lower scores

-

VA loans offer flexible credit requirements for eligible military buyers

If your credit needs improvement, don’t panic. Small steps like paying down debt and making on-time payments can help increase your score over time.

Step 3: Save for Upfront Costs

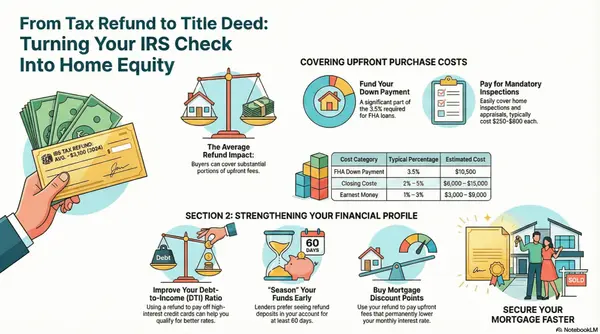

One of the biggest myths in real estate is that you need 20% down to buy a home.

In reality, many buyers purchase homes with much less.

Depending on the loan type:

-

FHA loans can require as little as 3.5% down

-

Conventional loans may allow 3% down

-

VA loans often require $0 down for qualified veterans and active-duty military

However, you should still prepare for:

-

Closing costs

-

Inspections

-

Earnest money deposit

-

Moving expenses

There are also first-time homebuyer assistance programs available in Texas that may help with down payment assistance.

Step 4: Get Pre-Approved

A pre-approval letter shows sellers you’re serious and financially qualified.

This step is especially important in competitive Texas markets like:

-

San Antonio

-

Austin

-

Dallas-Fort Worth

-

Houston

To get pre-approved, lenders typically review:

-

Income

-

Employment history

-

Credit score

-

Debt-to-income ratio

-

Bank statements

Once pre-approved, you’ll know exactly what price range to shop in.

Step 5: Find the Right Real Estate Agent

Working with an experienced real estate agent can make the process much smoother—especially for first-time buyers.

A good agent helps you:

-

Understand the market

-

Negotiate offers

-

Avoid costly mistakes

-

Coordinate inspections and deadlines

-

Navigate contracts and paperwork

If you’re a military family relocating during a PCS move, having an agent who understands VA loans and military timelines is incredibly valuable.

Step 6: Start House Hunting

Now comes the fun part—looking at homes.

As you tour properties, focus on:

-

Location

-

School districts

-

Commute times

-

Neighborhood safety

-

Future resale value

-

Condition of the home

It’s easy to fall in love with cosmetic features, but remember to think long-term.

Ask Yourself:

-

Will this home fit my needs in 3–5 years?

-

Is the neighborhood growing?

-

Are there major repairs needed?

Step 7: Make an Offer

Once you find the right home, your agent will help you submit an offer.

This includes:

-

Purchase price

-

Earnest money

-

Closing timeline

-

Contingencies

In competitive markets, negotiations can happen quickly. Your agent will guide you through counteroffers and help protect your interests.

Step 8: Schedule the Inspection

Never skip the home inspection.

Even beautiful homes can have hidden issues like:

-

Roof damage

-

Plumbing problems

-

Foundation concerns

-

HVAC issues

An inspection gives you peace of mind and may allow you to negotiate repairs or credits before closing.

Step 9: Final Loan Approval and Closing

After inspections and appraisal, your lender will finalize your loan.

Before closing, you’ll receive:

-

Final loan documents

-

Closing disclosures

-

Exact cash-to-close amount

On closing day, you’ll sign paperwork, receive the keys, and officially become a homeowner.

Common First-Time Homebuyer Mistakes to Avoid

Here are some mistakes many buyers make:

Making Large Purchases Before Closing

Avoid financing cars, furniture, or expensive items before your mortgage closes.

Skipping Pre-Approval

Looking at homes before knowing your budget can lead to disappointment.

Ignoring Additional Costs

Remember that homeownership includes maintenance and taxes.

Draining Your Savings

Keep an emergency fund after closing.

Special Advice for Military Families Using VA Loans

VA loans are one of the best benefits available to military service members and veterans.

Benefits may include:

-

No down payment

-

Competitive interest rates

-

No private mortgage insurance (PMI)

-

Flexible qualification requirements

If you’re PCSing to Texas, start planning early. Virtual tours, remote closings, and military-friendly agents can make the process much easier.

Is Buying Better Than Renting?

For many Texans, the answer is yes.

When you rent:

-

Your payment builds your landlord’s wealth

-

Rent often increases yearly

-

You gain no equity

When you buy:

-

You build equity over time

-

Your payment may become more stable

-

You create long-term financial opportunities

While buying isn’t right for everyone immediately, many renters are surprised to learn they may already qualify for homeownership.

Final Thoughts

Buying your first home in Texas may feel intimidating at first, but with the right guidance, it becomes much more manageable.

The key is having a plan, understanding your options, and working with professionals who genuinely want to help you succeed.

Whether you’re a first-time buyer, military family relocating to Texas, or renter dreaming of owning a home, taking the first step today can change your future for years to come.

If you have questions about buying a home in Texas, VA loans, or preparing for your first purchase, I’d be happy to help guide you through the process.

Categories

Recent Posts