Beyond the Bonus: 5 Strategic Ways Your Tax Refund Can Hack Your Path to Homeownership

1. Introduction: The High-Stakes Choice of Tax Season

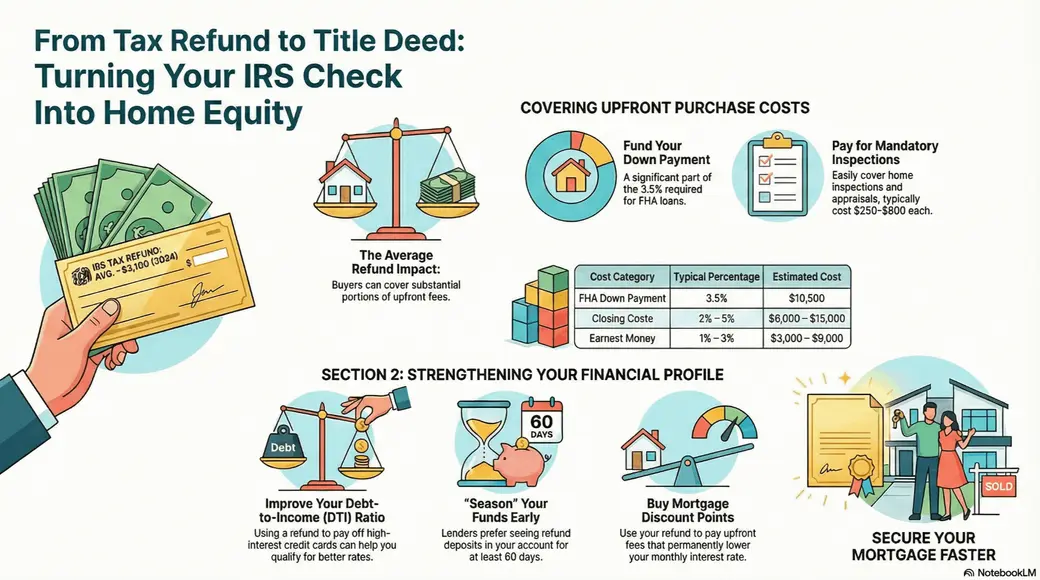

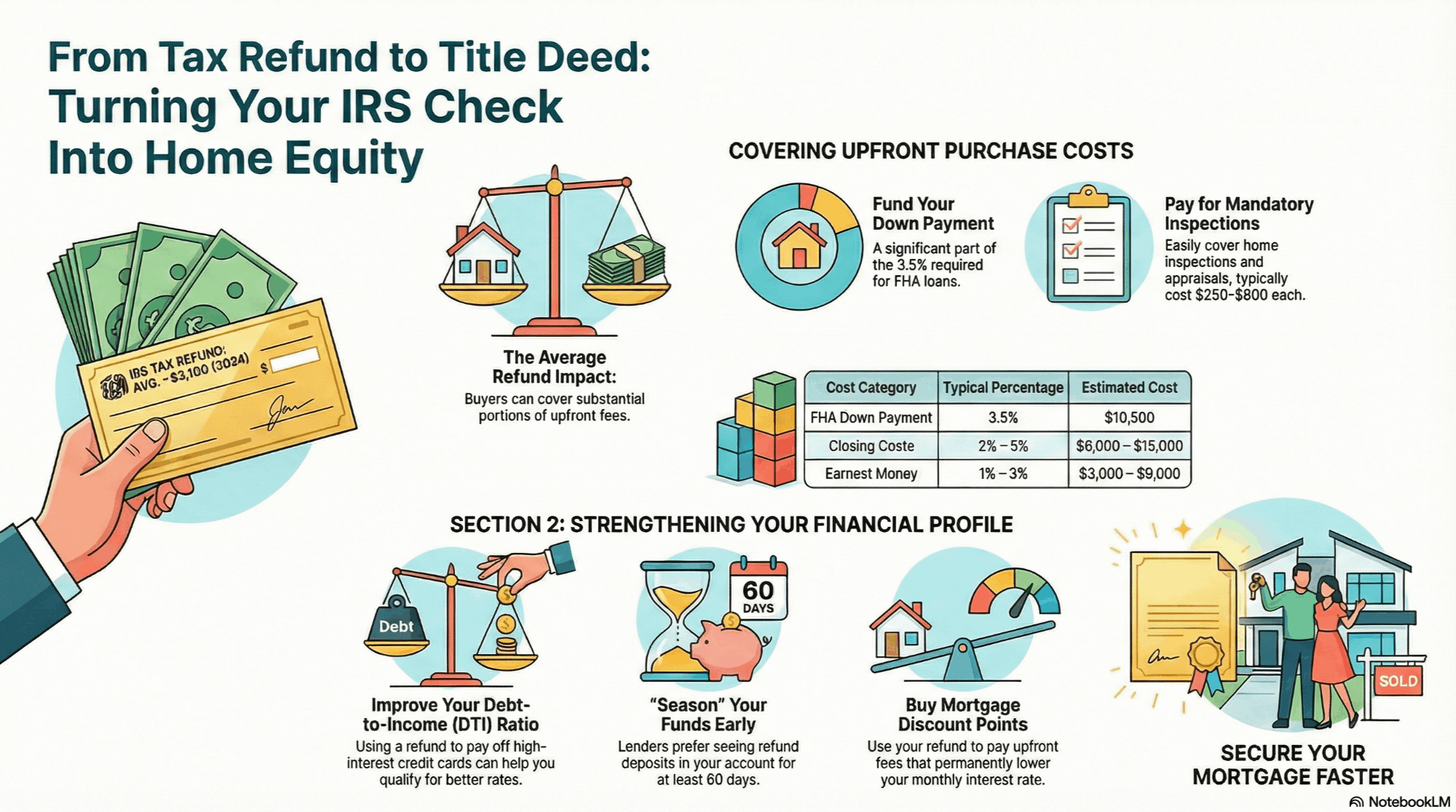

Tax season presents a critical inflection point for your financial trajectory. It is the moment of the "high-stakes choice": do you succumb to the immediate gratification of a "bonus" splurge—vacations, electronics, or retail therapy—or do you deploy that capital as a strategic catalyst for long-term wealth? For those targeting a home purchase in 2025 or 2026, the average federal refund (which ranged from $3,050 to $3,145 in 2024) is far more than a windfall; it is a force multiplier for your real estate goals.

According to data from the National Association of Realtors (NAR), 26% of first-time homebuyers successfully utilized their tax refunds as a cornerstone of their acquisition strategy. By viewing this liquidity through the lens of a Senior Strategist, you can transform a one-time check into the foundation of a primary residence.

2. Myth-Busting the 20% Down Payment Barrier

The "20% down" requirement is a persistent myth that prevents many qualified buyers from entering the market. While 20% is the threshold to avoid Private Mortgage Insurance (PMI), waiting to save that amount in a rising market often results in lost equity growth that far outweighs the cost of the insurance.

Strategically deploying your refund as "asset seasoning" allows you to exploit entry-level loan products with significantly lower cash requirements. Lenders prioritize "seasoned funds"—money that has been documented in your account for at least 60 days—to satisfy anti-money laundering protocols and verify that the capital is not an undisclosed loan. Your tax refund, properly documented, is the ultimate "clean" source of funds.

Refund Impact on a $300,000 Home:

|

Loan Type |

Minimum Down Payment % |

Required Cash Amount |

|

VA Loan |

0% |

$0 |

|

USDA Loan |

0% |

$0 |

|

Conventional 97 |

3% |

$9,000 |

|

FHA Loan |

3.5% |

$10,500 |

"If you plan well, your refund can be a key part of how you pay for a home. You can add it to a down payment, pay for closing costs, or cover inspections and appraisals."

3. Exploiting the Federal Reserve’s "Savers Runway"

The current macroeconomic environment has gifted prospective buyers a unique "savers runway." At the March Federal Reserve meeting, officials declined to cut interest rates, citing economic uncertainty—including potential impacts from impending tariffs. For the homebuyer, this uncertainty is an opportunity. Higher-for-longer rates mean that High-Yield Savings Accounts (HYSAs) continue to offer exceptional returns on your parked capital.

To maximize your refund’s growth while maintaining the liquidity needed to move fast on a listing, avoid the rigidity of a CD and utilize an HYSA. Current market leaders include:

- Poppy Bank: 4.40% APY

- My Banking Direct: 4.40% APY

- Newtek Bank: 4.35% APY

- Western Alliance Bank: 4.30% APY

This strategy ensures your funds outpace inflation while remaining "at the ready" for when the right property hits the market.

4. The "Hidden" ROI: Improving Your Debt-to-Income (DTI) Ratio

As a strategist, you must recognize that your refund may be more powerful when used to pay down debt than when added to a down payment. Lenders use your Debt-to-Income (DTI) ratio to determine your borrowing capacity.

While a $3,000 addition to a down payment only increases your purchase price by $3,000, using that same $3,000 to eliminate a high-interest credit card or personal loan could lower your monthly debt obligations enough to increase your qualifying loan amount by tens of thousands of dollars. Improving your DTI doesn’t just help you get the loan; it secures a more favorable interest rate and ensures your monthly amortization remains sustainable over the life of the mortgage.

5. The Dollar-for-Dollar Power of Mortgage Tax Credit Certificates (MCC)

First-time buyers—defined as those who have not owned a principal residence in the last three years—can leverage the Mortgage Tax Credit Certificate (MCC) to turn mortgage interest into a direct tax asset.

Unlike a tax deduction, which reduces taxable income, an MCC is a dollar-for-dollar credit against your federal tax liability.

- The Benefit: Claim a credit for 20% to 40% of your annual mortgage interest.

- The Cap: The IRS limits this credit to a maximum of $2,000 per year.

- The Strategy: By amending your W-4 withholdings, you can receive this benefit in your monthly paycheck, effectively increasing your qualifying income for the lender.

Special Note: To avoid a "recapture tax," the property must remain your primary residence. Selling the home within the first nine years may trigger a partial repayment of the credit to the IRS if your income has significantly increased.

6. State-Level Strategic Advantages: The Maryland Model

Forward-thinking buyers should investigate state-specific vehicles like the Maryland First-Time Homebuyer Savings Account (FHSA). This model allows residents who haven’t owned a home in Maryland for 7 years to compound their refund’s value through tax-advantaged growth.

- Annual Benefit: A state tax subtraction of up to $5,000 per year.

- Lifetime Cap: A total subtraction of $50,000 over a 10-year period.

- Strategic Compounding: These accounts allow for the inclusion of "gift funds." By adding your tax refund to gifts from family within this structure, you create a tax-shielded engine that accelerates your path to the closing table.

7. Conclusion: Timing the Market with Your Refund

In real estate, timing is the difference between a successful acquisition and a bidding-war loss. Expert market analysis suggests that the optimal window to deploy your refund is Q2 (April/May). By acting early in the spring, you utilize your liquidity before the "summer rush" price wars begin and inventory becomes hyper-competitive.

Your tax refund is a rare moment of discretionary liquidity. Will it be a fleeting memory of a vacation, or will it be the seasoned foundation of your first home? The choice is the difference between being a renter and becoming an owner.

Categories

Recent Posts